Fabric alone accounts for 60–70% of the total cost of a basic garment. Yet many apparel brands still build their cost sheets in spreadsheets. These break the moment a supplier changes a price, sending the entire pricing structure out of date. In fact, garment costing is not just an accounting exercise. Indeed, it is the financial foundation of every product decision your brand makes — from factory selection and production volumes to wholesale and retail pricing.

In particular, this guide walks through every component of garment costing. It covers the difference between CMT and FOB pricing, how to build a reliable cost sheet, and how modern PLM software keeps costs accurate as your product evolves.

What Is Garment Costing?

In other words, garment costing is the systematic process of calculating the total cost to produce one unit of a finished garment. In particular, it starts with raw materials and finishes with a landed cost that reflects everything required to get that unit to your warehouse — fabric, labor, trims, freight, duties, and a share of factory overhead.

Moreover, an accurate cost sheet serves three purposes. First, it tells you whether a design is financially viable before you commit to sampling. Second, it gives you the data to negotiate with suppliers from an informed position. Third, it determines your minimum viable wholesale and retail prices.

Above all, apparel costing is also ongoing. At the sketch stage, cost is an estimate. After lab dip approval, it becomes more accurate. Only after bulk fabric confirmation can your finance team therefore rely on the number. Brands that treat costing as a one-time calculation routinely absorb margin surprises at production sign-off. Instead, a cost sheet should be a living document tied to product development — not a file that gets completed once and forgotten.

What Are the Main Components of a Garment Cost Sheet?

A complete garment cost sheet captures every expense category from raw material to your dock. The table below shows the standard line items and what they represent.

| Cost Component | What It Includes | Typical Share of Total Cost |

|---|---|---|

| Fabric | Shell, lining, interlining — calculated by yield (meters per unit) × price per meter | 50–70% |

| Trims & findings | Zippers, buttons, labels, hang tags, elastic, threads, packaging | 5–15% |

| CMT labor | Cut, Make, Trim fee — the factory’s charge for converting materials into a finished garment | 15–25% |

| Factory overhead | Machine depreciation, utilities, quality control staff — either itemized or rolled into the CMT rate | Included in CMT or 3–8% |

| Freight & handling | Sea or air freight, origin charges, inland transport to port | 3–8% |

| Duties & tariffs | Import duties based on HS code and country of origin | 0–20% depending on trade agreements |

| Landed cost (CMC) | All of the above combined — the total cost to get one unit to your warehouse | 100% baseline |

| Wholesale price | Landed cost × 2.0–2.5 (keystone or higher depending on category) | Markup target |

| Retail price | Wholesale price × 2.0–2.5 (standard keystone for most brands) | Markup target |

The bill of materials (BOM) feeds directly into the fabric and trim rows. If your BOM is managed inside a PLM system like Wave PLM, changes to material specs automatically flow through to the cost sheet — eliminating the manual syncing that spreadsheets require.

CMT vs FOB: Which Costing Method Should You Use?

In particular, the two most common production frameworks are CMT and FOB. As a result, these two models cover the vast majority of production arrangements in apparel. Therefore, understanding the difference determines how you structure supplier relationships and where your cost exposure sits.

CMT (Cut, Make, Trim) means the brand is responsible for sourcing and delivering all fabrics and trims to the factory. In particular, the factory charges only for labor — cutting, sewing, finishing, and trimming. CMT gives brands maximum control over material quality and supplier relationships. However, it does require a dedicated sourcing team or agent to manage fabric procurement and logistics.

Alternatively, FOB (Free On Board) means the factory handles both materials and labor, delivering a finished garment to the origin port. Furthermore, FOB simplifies procurement significantly and works well for brands without in-house sourcing infrastructure. However, the factory controls material quality and margins on raw goods.

| CMT | FOB | |

|---|---|---|

| Who buys fabric | Brand | Factory |

| Material control | High | Lower |

| Costing complexity | Higher (more line items) | Lower (one price) |

| Margin visibility | Full transparency | Limited (factory margin hidden) |

| Suitable for | Brands with sourcing team, 500+ units per style | Early-stage brands, simpler styles, tight timelines |

A common approach for growing brands is to start with FOB and migrate key hero styles to CMT as supplier relationships and internal sourcing capability mature. In both cases, the spec sheet and BOM remain the documents the cost sheet is built from — so accuracy at the spec stage compounds into accuracy at costing.

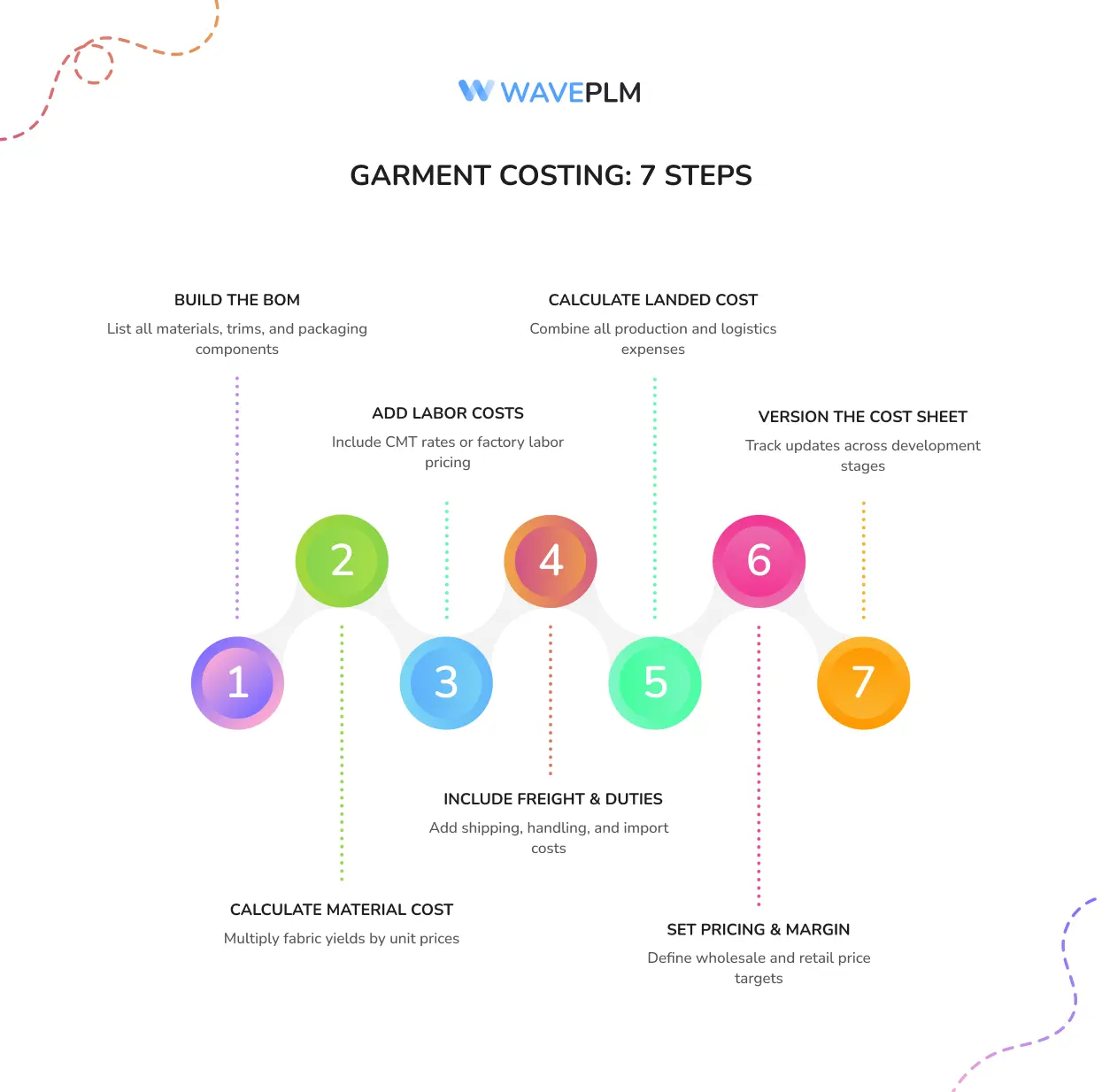

How Do You Build a Garment Costing Sheet Step by Step?

The process below applies whether you work in a spreadsheet or a PLM system. The difference is how much of it is automated and how current the data stays.

Step 1 — Start with the BOM. List every material the garment requires: shell fabric, lining, interlining, zipper, buttons, labels, hang tag, poly bag. For each item, record the supplier, unit of measure, price, and yield (how much material you need per finished unit including waste allowance).

Step 2 — Calculate material cost per unit. For fabric: multiply yield (e.g., 1.4 meters) by price per meter (e.g., $4.80) = $6.72 fabric cost per unit. Repeat for every BOM line and sum to get total material cost.

Step 3 — Add CMT or labor cost. If CMT, use the factory’s quoted rate for this style (complexity, number of operations, and target country determine this). If FOB, the labor cost is already embedded in the factory price — note it separately for benchmarking if possible.

Step 4 — Layer in overhead and freight. If your factory quotes FOB, freight begins at the origin port. Add sea freight, destination handling, and inland transport. Apply the relevant duty rate for your HS code and country of origin.

Step 5 — Calculate your landed cost (CMC). Sum all rows above. This is your cost of manufacture at your warehouse door.

Step 6 — Apply margin and set pricing. Use your target margin to calculate minimum wholesale and retail prices. Document the margin percentage and review against your category benchmark.

Step 7 — Version and date the sheet. Every time a material price, yield, or labor rate changes, create a new version. Cost Version 1 (sketch), Cost Version 2 (after proto), Cost Version 3 (after bulk fabric confirmation) are meaningfully different documents.

Wave PLM note: In Wave PLM, cost sheets are linked directly to the tech pack and BOM. When a sourcing manager updates a fabric price, the cost sheet recalculates automatically and the change is logged with a timestamp. Design, sourcing, and production teams always see the same current cost — not the version from last month’s email thread.

What Are the Most Common Garment Costing Mistakes?

In short, costing errors are not about misunderstanding the formulas. Instead, they almost always stem from stale data or a missing cost category. In short, the most common mistakes apparel brands make are as follows.

Underestimating fabric yield

In particular, fabric yield — how much material you actually consume per unit — varies by fabric width, pattern placement, and cutting efficiency. As a result, brands that use round numbers without measuring actual consumption routinely find fabric costs 15–20% higher than budgeted.

Ignoring trim and packaging costs

For example, a zipper, a set of buttons, a label, a hang tag, and a poly bag can add $1.50–3.00 per unit on a garment that costs $8.00 to make. Therefore, omitting or underestimating these is the second most common source of margin leakage.

Forgetting duties and tariffs

Indeed, import duty rates vary dramatically by product category and country of origin. For instance, a knit sweater and a woven jacket have different HS codes and different duty rates even from the same factory. Consequently, brands sourcing from multiple countries often apply a single blanket duty estimate and absorb real differences at customs. See the full guide to customs tariffs in U.S. fashion for category-specific rates.

Using the proto sample cost for production

In particular, proto samples are typically hand-made in small quantities — they do not reflect bulk production labor rates, material minimums, or yield efficiencies. For example, a garment that costs $18 in proto can cost $11 at production scale, or $22 if the factory encounters unexpected complexity. Therefore, always request a fresh costing after bulk material confirmation.

Not versioning cost sheets

When a cost sheet exists as a single tab in a shared spreadsheet, anyone can overwrite it. Furthermore, brands that do not track cost versions lose the ability to understand why their margin changed between seasons. Moving faster without version control amplifies this risk.

How Does PLM Software Improve Garment Costing?

Spreadsheet costing is functional at low volumes. Yet it breaks at scale — when a brand has 80+ styles per season, multiple factories across different regions, and a team where design, sourcing, and production work in different tools.

As a result, PLM software solves the core problem of garment costing: scattered data. In short, it links every cost input to one source of truth. Here is what connected costing looks like in practice inside Wave PLM.

BOM-linked cost rollup

Instead of manually copying material prices into a cost sheet, the cost sheet reads directly from the BOM. When a sourcing manager confirms a fabric at $5.20 per meter instead of the estimated $4.80, the cost sheet updates automatically. As a result, everyone on the product team sees the change in real time.

Scenario comparison

For instance, Wave PLM lets teams run CMT and FOB scenarios side by side on the same style. For example, if Factory A quotes CMT at $6.50 and Factory B quotes FOB at $14.00, consequently the system calculates which is actually cheaper after adding material sourcing costs, freight, and duty — making the comparison apples to apples rather than apples to oranges.

Cost versioning alongside design versioning

In particular, cost sheets link directly to tech pack versions. For example, version 3 of the tech pack has its own Cost Sheet V3. If a designer reverts to an earlier construction, the cost associated with that construction is also visible. As a result, this is critical for understanding the cost impact of design changes.

Factory visibility without email

With Wave PLM, factories and suppliers can see the cost sheets relevant to their orders directly, without receiving spreadsheet attachments. Consequently, this eliminates version confusion and the common problem of factories quoting against outdated specs. It also connects to multi-factory coordination workflows where cost comparisons across vendors need to happen quickly.

For brands implementing PLM for the first time, costing often delivers the fastest return. In fact, the status quo — email and spreadsheets — is the most expensive workflow to maintain at scale. If you are evaluating PLM options, the PLM implementation guide covers how to roll out cost management as part of a phased deployment.

Key Takeaways for Accurate Garment Costing

In summary, accurate garment costing requires current data, proper versioning, and a process that updates the cost sheet whenever the product changes — not just at the end of the development cycle. Therefore, the main points to carry forward are these:

First, fabric is your largest cost driver at 50–70% of garment cost, and yield accuracy is the single biggest variable that separates estimated cost from actual cost. Additionally, CMT gives you more material control; FOB simplifies operations but hides factory margins. Moreover, cost sheets should be versioned alongside tech packs, not maintained as a single overwritten file. Finally, duties and tariffs are not optional line items — they can swing landed cost by 15–20% depending on product category and sourcing country.

If your team is still reconciling cost sheets manually against BOM updates, therefore, book a Wave PLM demo to see how connected costing works in practice — from first estimate to production sign-off.

Frequently Asked Questions

What is garment costing?

Simply put, garment costing is the systematic process of calculating the total cost to produce a single unit of clothing — from raw materials and labor through factory overhead, freight, duties, and target margin. As a result, an accurate cost sheet lets apparel brands set profitable wholesale and retail prices before committing to production.

What is the difference between CMT and FOB in garment costing?

In particular, CMT (Cut, Make, Trim) is the fee charged by a factory for labor only — the brand supplies all fabrics and trims. In contrast, FOB (Free On Board) is a full-service price that includes materials, labor, factory overhead, and delivery to the origin port. Whereas CMT gives brands more material control, FOB simplifies vendor management for brands without dedicated sourcing teams.

What percentage of garment cost is fabric?

Mainly, fabric accounts for 60–70% of the total cost of basic-styled garments. For fashion-forward or heavily detailed styles, however, trims and embellishments can shift that share, but fabric nonetheless remains the single largest cost driver in most apparel categories.

How does PLM software help with garment costing?

In particular, PLM software links your costing sheet directly to the BOM, so any change to a fabric price, trim, or yield automatically recalculates the cost. As a result, teams can compare CMT vs FOB scenarios side by side, track cost versions alongside design versions, and share live cost data with factories — replacing manual spreadsheet reconciliation with a connected workflow.

Leave a Reply